Understanding Key Financial Statement Ratios

Oftentimes investors and managers need to look beyond raw data on financial statements to understand a company’s financial health. Financial ratios help achieve this by simplifying complex data and making it easier to compare companies and track performance over time.

By analyzing relationships across financial statements, ratios provide insight into how profitable a company is, how well it manages its resources and obligations, and how efficient it operates. Financial ratios are commonly grouped into four main categories that each highlight a different aspect of a company’s financial performance: profitability, liquidity, leverage, and efficiency.

Profitability Ratios

Profitability ratios measure how effectively a company generates profit from its revenue and operations. These ratios help investors understand whether a company is turning its sales into actual earnings.

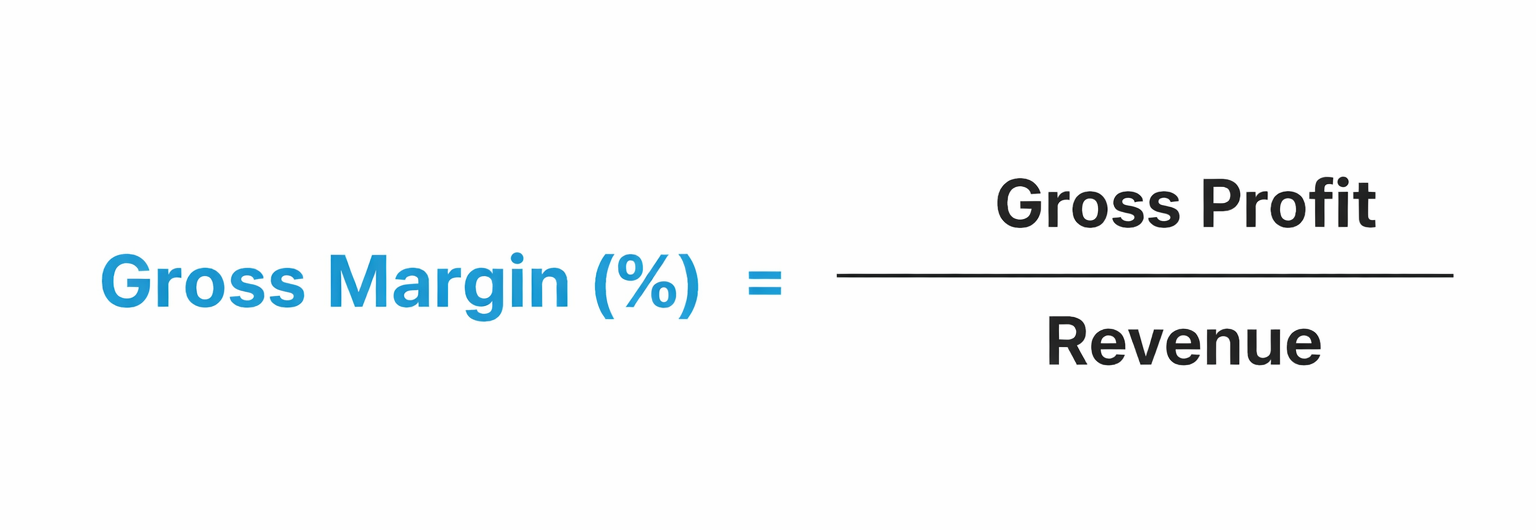

Gross Profit Margin shows how much profit remains after subtracting the cost of producing goods or services. It measures how efficiently a company manages production costs.

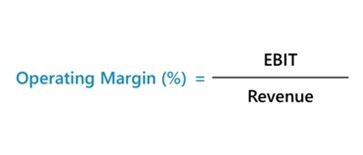

Operating Profit Margin evaluates how profitable a company’s core operations are after accounting for operating expenses such as salaries, rent, and utilities.

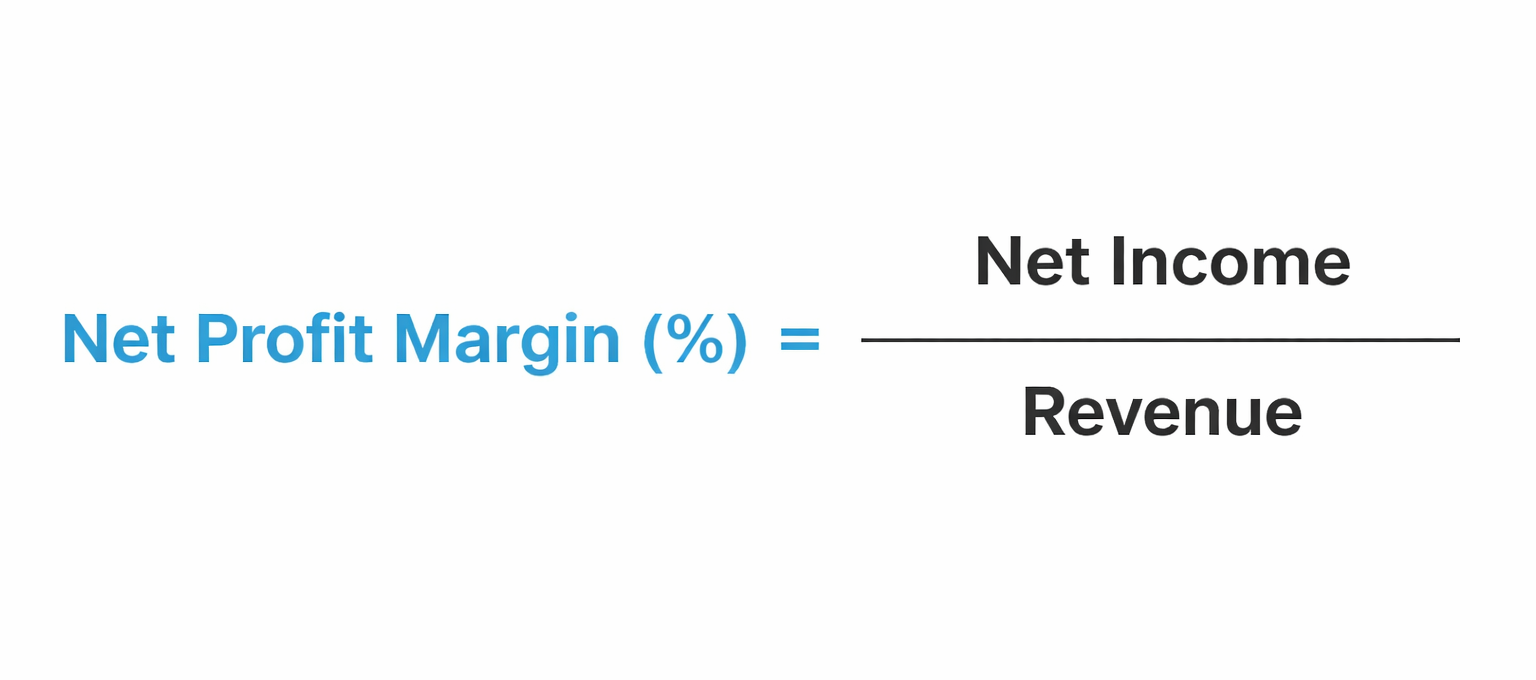

Net Profit Margin reflects the percentage of revenue that remains as profit after all expenses, taxes, and interest are paid. This ratio provides a clear view of a company’s overall profitability.

Higher profitability margins generally indicate stronger financial performance and better cost management.

Liquidity Ratios

Liquidity ratios measure a company’s ability to meet its short-term financial obligations. These ratios are important when assessing whether a business has enough resources to pay its upcoming bills.

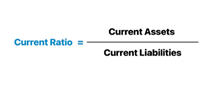

Current Ratio compares a company’s current assets to its current liabilities. It indicates whether the company has enough short-term assets, such as cash, inventory, or receivables, to cover its short-term debts.

A higher current ratio suggests stronger short-term financial stability, though extremely high values may also indicate that resources are not being used efficiently.

Leverage Ratios

Leverage ratios evaluate how much a company relies on borrowed money to finance its operations. These ratios help investors understand the level of financial risk associated with a company’s capital structure.

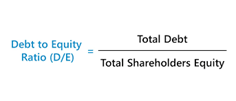

Debt-to-Equity Ratio compares a company’s total debt to shareholders’ equity. It shows how much financing comes from creditors versus owners.

Companies with higher debt-to-equity ratios rely more heavily on borrowed funds, which can increase risk during economic downturns. However, some leverage can also help companies grow by allowing them to invest in new opportunities.

Efficiency Ratios

Efficiency ratios measure how effectively a company uses its assets and resources to generate revenue.

Inventory Turnover shows how quickly a company sells and replaces its inventory over a period of time. A higher inventory turnover generally indicates strong sales or efficient inventory management.

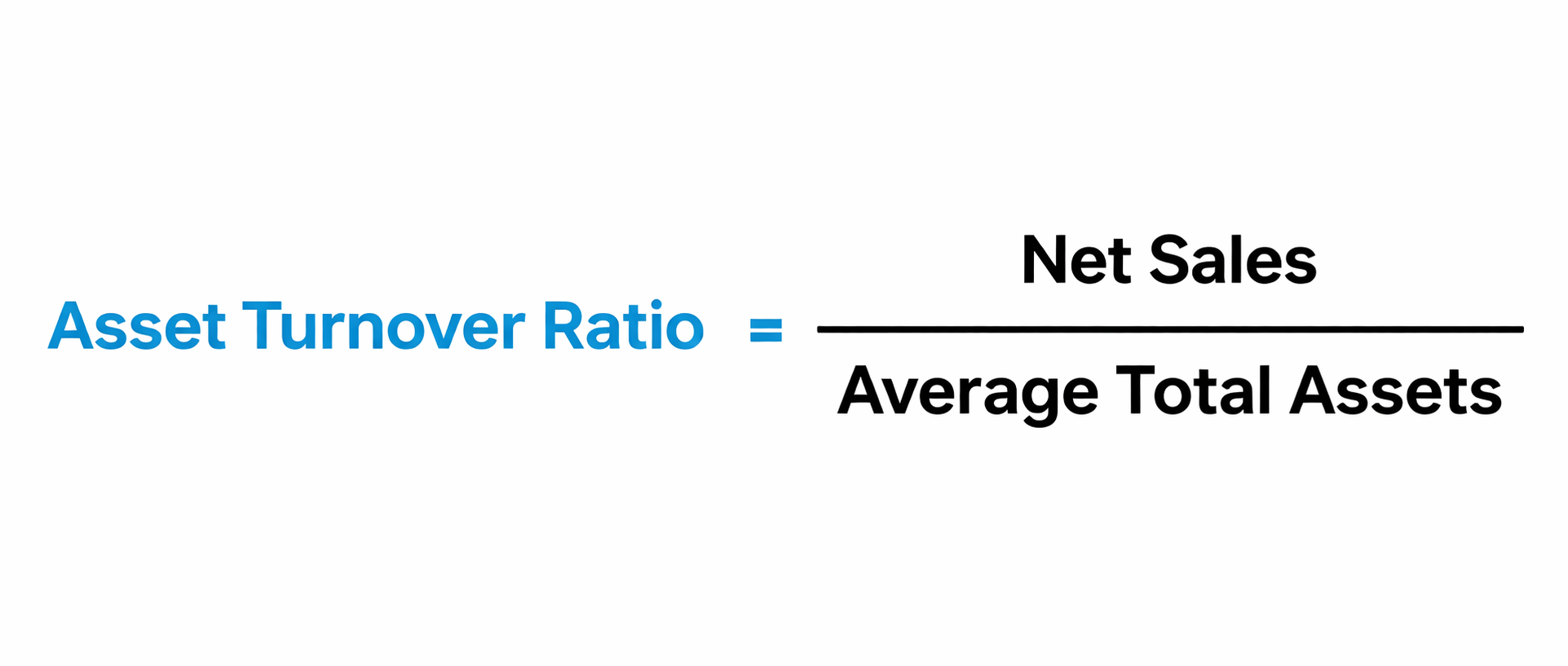

Asset Turnover measures how efficiently a company uses its total assets to generate revenue. Companies with higher asset turnover ratios are typically better at using their resources to produce sales.

These ratios help identify whether a company is maximizing the productivity of its assets.

Why Financial Ratios Matter

Financial ratios provide a clearer picture of a company’s performance by turning financial data into meaningful and complex relationships. By understanding profitability, liquidity, leverage, and efficiency, investors and managers can better evaluate a company’s strengths, weaknesses, and long-term sustainability.